Is Manchesterism working?

And what is actually existing Manchesterism?

Investigations into why Greater Manchester has been successful in recent decades are very popular at the moment.1 However, some have questioned whether Greater Manchester really has been that successful after all. Others have argued that Greater Manchester’s growth somehow does not count because it has been focused in and around the centre of the conurbation.

The evidence suggests a more balanced conclusion. Greater Manchester is not Britain’s top-performing city region. Bristol, and particularly Edinburgh, have consistently outperformed it in recent decades. However, the broader claim that Greater Manchester has not outperformed most other British cities on a per capita basis is probably wrong, and tends to rest on an overly narrow reading of the data. Taking the evidence as a whole, Greater Manchester is one of the stronger performers, though the data is messy. If Greater Manchester’s population growth is allowed to count in its favour, as it should be, then its status as one of the strongest city-region performers after Edinburgh and Bristol becomes much clearer.2

The data also makes it clear that Greater Manchester’s growth has been focused on the centre of the conurbation. But that is a feature of the model, not a bug. Criticising Greater Manchester’s growth model on the basis that growth has been concentrated in and around the City of Manchester misunderstands both the region’s recent history and the economics of agglomeration.

Greater Manchester’s per capita performance is pretty good

There are many different ways to measure the relative success of regional economies. What matters for present purposes is growth relative to similar economies. Greater Manchester has been richer than Liverpool for some time. Greater Manchester has been poorer than Oxfordshire for some time.

But if Greater Manchester is doing relatively well, its living standards should be pulling further clear of places like Liverpool and catching up with places like Oxfordshire. The important thing to look at then is not ‘how rich is Greater Manchester compared to other places’ but how fast it is growing compared to other city regions.

Overall, the data suggests that Greater Manchester has probably grown faster per person than most other British city regions, though Bristol and especially Edinburgh have performed much more strongly.

GDP per capita is the economic output per head of the region. Greater Manchester performs strongly, though Liverpool, starting from a much lower base, Bristol, and especially Edinburgh have outperformed Greater Manchester by this metric.

GVA per capita is the value generated by producers in an area, calculated as output minus intermediate inputs, divided by the local population. It is similar to GDP but while GDP includes product taxes (mostly VAT in the UK) but does not include product subsidies, GVA is the other way round. Greater Manchester again does well, with Bristol performing slightly better and Edinburgh again by far the strongest performer.

Gross Disposable Household Income per capita is the amount of money households have available to spend or save after taxes, social contributions, and benefits are accounted for, divided by the population. It is useful because it captures how much income actually reaches households, rather than just how much output is produced in an area. On this metric, Greater Manchester does worse than most other cities.

So which figure is right? One possible explanation is that Greater Manchester’s output figures increasingly reflect people who work in or visit the city region but do not live there. That would boost GDP and GVA relative to resident household income. However, the available long-run data is not good enough to prove this.

If someone lives in Preston or Macclesfield but works in Deansgate, the GDP and GVA they produce at work will count towards Greater Manchester’s figures. However, it will not add much to Greater Manchester’s gross household income figures, as these are calculated based on income received by residents and allocated to where people live.

Unfortunately, there is not a good way to tell how commuting or tourism has changed across Britain’s major cities in recent decades. The 2011 census counted commuters into and out of major cities, but this was the first time it had done so. The 2021 census was conducted during Covid, so it was decided that these figures would not be useful to collect. There are data on railway station users and congestion, but these do not reveal whether the journeys are people coming into the city for work and leisure, going out for work and leisure, or simply moving within the city region. For present purposes, that is not useful enough.

Greater Manchester improving its position relative to other cities at attracting commuters and visitors is therefore a possible explanation for its GDP and GVA figures looking better than its household disposable income figures. But there is no strong evidence either way.

Tax and benefits

Another possible explanation is tax and benefits. For GVA and GDP figures, if someone earns income that is then taxed and spent on benefits elsewhere, that activity is counted where the output is generated, that is, where the worker works. However, for household disposable income figures, benefit income is counted where the benefit recipient lives.

A place becoming more successful economically will therefore have some of its success obscured in the household income figures by the progressive tax and benefits system. As people increase their incomes, they receive fewer benefits and pay more tax. Their household income therefore rises more slowly than the area’s GDP.

The DWP publishes detailed figures on benefit spending by local authority area going back to 2002. For Scotland, these figures are not comparable over time, as more benefits have been devolved to Scotland since then. But for England and Wales, it is possible to compare different cities’ growth in household incomes since 2002 both with and without benefits. HMRC also has tax data by local authority, but only back to 2010. I have therefore included two graphs: one that adjusts for benefit spending back to 2002, and one that adjusts for taxation and benefit spending back to 2010.

As these adjustments show, Greater Manchester performs much better once tax and benefits are accounted for. As should be expected by now, Greater Manchester is still behind Bristol. However, it also remains behind several other cities. Greater Manchester is in the middle of the pack, but importantly for present purposes it outperforms several of its most directly comparable city regions, including Liverpool, the West Midlands, and West Yorkshire.

Data problems

So far, the evidence suggests that commuting and tourism might explain some of the discrepancy between Greater Manchester’s GVA and GDP figures and its GDHI figures, but there is no strong evidence either way. Tax and benefits likely explain a significant part of the difference, but not all of it. Looking at how the data is constructed does not provide an obvious answer for where the rest of the difference comes from. (I discuss this in more detail in the footnotes.)3

However, there is no obvious reason to think that the GVA figure is clearly better constructed than the GDHI figure, or vice versa. The reasonable conclusion is that Greater Manchester’s per capita performance depends partly on which measure is given the most weight.

On the output measures, Greater Manchester looks like one of the strongest performers after Edinburgh and Bristol. On household income, it looks more middle of the pack, though still ahead of many comparable large northern and Midlands city regions. Reasonable people can disagree about which measure deserves more weight, but it is hard to sustain the claim that Greater Manchester has not performed relatively well.

Quantity has a quality of its own

So far, this piece has focused on Greater Manchester’s per capita performance. But this is not the only relevant measure of success. Successful cities do not just grow the incomes of people who are already there. They bring new people in and make people who are from there want to stay.

When comparing independent countries, looking mainly at per capita figures makes sense. Countries have very different immigration policies and national birth rates will do more to explain population growth than economic success or failure. But for cities within the same country, with the same immigration policy and broadly similar birth rates, more successful places should be expected to attract and retain more people.

It is therefore also worth looking at overall growth rates without adjusting for population.

In GDP terms, a familiar pattern emerges: Greater Manchester performs very well but is outperformed by Edinburgh and Bristol.

As before, household income, even excluding benefits, is less favourable to Greater Manchester. But Greater Manchester still performs well.

The regions containing Oxford and Cambridge and Nottingham overtake Greater Manchester, but Greater Manchester still performs better than all of the other cities in the north and Midlands. Taking out benefits, Manchester does even better. Due to devolution, Scottish cities cannot be compared on this metric.

Adding in an adjustment for taxation and comparing back to 2010 shows a similar story, with Greater Manchester performing well but southern cities outperforming it.

This data gives greater confidence that Greater Manchester has been a strongly performing economy in recent decades, albeit not as strong as Edinburgh or Bristol. By some metrics, Oxford and Cambridge outperform Greater Manchester and the region containing drawing essentially level by one metric. However, there can be reasonably high confidence that Greater Manchester is the best-performing city region in the north and Midlands of England, and on some metrics it is even outperforming the regions containing Oxford and Cambridge.

Greater Manchester’s growth is in the city centre. Economics and history show this is the right strategy.

It is possible to see where Greater Manchester’s growth is happening. On a clear day, it can even be seen from 33 miles away in Liverpool with a decent phone camera.

It is also clear in the data. As recently as 2005 there was just one building over 100 metres tall in Greater Manchester and only 4 in 2017. There will soon be 30.

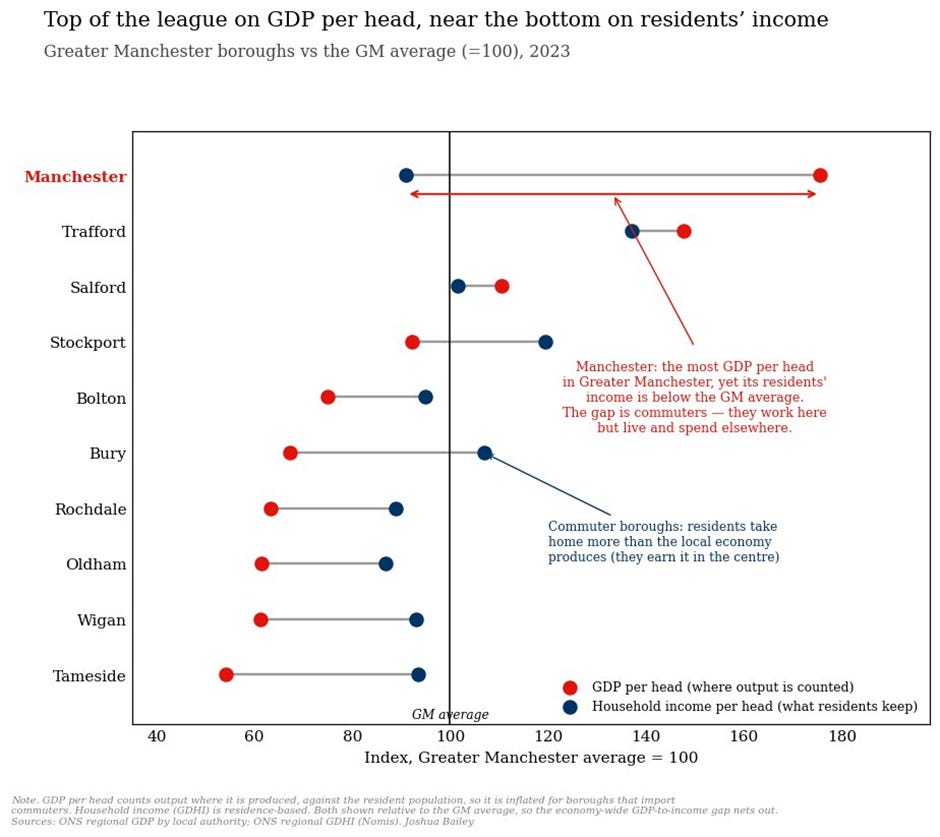

It shows up in the economic data too. The City of Manchester’s household disposable income has grown far faster than other parts of Greater Manchester.

Housing delivery tells the same story. Greater Manchester as a whole is, like all English city regions, far short of its housing targets.

The City of Manchester, though, is building a huge amount. All of the other major city cores have a substantial amount of work to do to meet their housing targets. The City of Manchester does not.

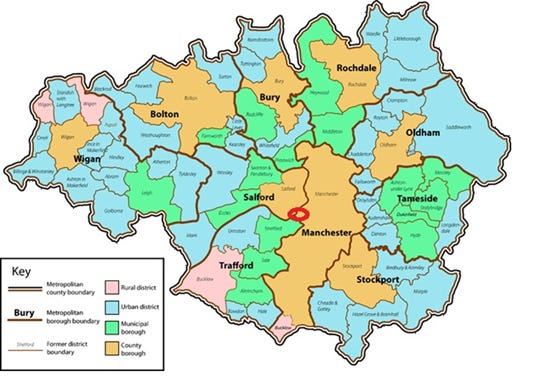

Greater Manchester’s leaders have made a conscious decision to build in the centre of the region. This becomes even more apparent when looking more precisely at where housing has been built within Greater Manchester. The City of Manchester is an odd shape, long and thin through the centre and south of the Greater Manchester region. The city centre is roughly where the red circle is.

Forty-five per cent of the City of Manchester’s population increase since 2001 has occurred within a 15-minute walk of the city centre. Including parts of Salford and Trafford within a 15-minute walk of the city centre, the population increased by over 120,000 between 2001 and 2023. This accounts for 23% of Greater Manchester’s population increase occurring on just 2% of its land mass.

Greater Manchester’s leaders are clearly encouraging building in the city centre. This is occasionally criticised for prioritising the City of Manchester over the rest of Greater Manchester and leaving other parts of the region behind. This criticism misunderstands both recent Greater Manchester history and recent global economic history.

On local history, as recently as 2015 the City of Manchester had the lowest household incomes of any of the Greater Manchester boroughs. It used to be far behind the other nine. It is still only eighth out of ten, ahead of only Oldham and Rochdale. People in Stockport have household disposable incomes 31% higher per head than people in the City of Manchester, and in Trafford the figure is over 50% higher. Focusing growth on one of the poorest parts of the conurbation can hardly be called leaving everywhere else behind.

This criticism often highlights the fact that the City of Manchester’s GDP is higher than that of the surrounding boroughs. But that fails to take into account the fact that many people across Greater Manchester commute into the centre for work. Salford, a borough that contains parts of the city centre also has higher GDP than household income, as does Trafford which is adjacent to the City Centre and contains a very large industrial estate.

Those who argue that towns like Wigan and Oldham have done less well than central Manchester have something of a point. They have not grown as fast as the city centre. But what they often do not have is a credible alternative growth model. Economic growth is not something politicians can simply assign to different parts of a region or country. It needs a mechanism. The plan Greater Manchester has followed, under Andy Burnham’s leadership and long before, has worked.

It is also a plan that goes with the flow of economic development in the developed world since the 1990s. Rich country economies have shifted away from a world in which the richest places were driven mainly by large amounts of physical capital: factories, machinery, and heavy infrastructure. Increasingly, growth has come from ideas, software, design, finance, professional services, management know-how, and other intangible assets.

These intangible assets behave differently from physical ones and need different things to succeed. From the 1930s to the 1970s, Britain’s great cities, including London, emptied out, with the cutting edge of the economy moving to small-town and out-of-town industrial and engineering parks. In recent the decades the cutting edge of the economy has been moving back to city centres, especially in London, Edinburgh, Bristol and the centre of Greater Manchester.

This is because intangible assets are often scalable, spill over between firms, and become more valuable when combined with other ideas and skills. That makes proximity between firms and between people much more important. A factory can often be placed on cheap land outside town and still work perfectly well. A cluster of software engineers, investors, lawyers, designers, founders, accountants, researchers, and clients works best when people can meet, change jobs, copy ideas, form firms, and learn from each other quickly.

Better roads and better public transport can help by making a wider labour market function more like one place. But the simplest and most powerful way to achieve this is still to allow lots of people to live and work close together. This is why the centres of big cities have made a comeback across the developed world. Greater Manchester’s strategy of building lots of homes in and around the centre of the conurbation is not a weird fixation of its leaders. It is going with the grain of the global economy. And it has worked.

Greater Manchester refers to the city region made up of ten local authority areas: Bolton, Bury, Manchester, Oldham, Rochdale, Salford, Stockport, Tameside, Trafford, and Wigan. The City of Manchester refers only to one of those ten local authority areas. The city centre extends beyond the City of Manchester local authority boundary into parts of Salford and is adjacent to Trafford.

I have aimed to cover all regions of Britain with an urban population of over 400,000. I have also included Oxford and Cambridge as they are often cited as potential growth engines for the UK by national level politicians. City regions in England are defined by Mayoral Combined Authorities where possible. For Oxford I have used the Oxfordshire County Council area. For Cardiff I used the Cardiff Capital Region. For Glasgow I used the region ‘Glasgow and Strathclyde’ and for Edinburgh I used ‘Edinburgh and the Lothains. There are some differences in areas considered for the GVA stats due to data limitations where the Liverpool City Region figures exclude the borough of Halton, the Edinburgh figures include Falkirk and the Glasgow figures exclude Ayrshire and South Lanarkshire.

GDP figures are derived from the GVA figures with some extra tax data. Regional GVA is mainly estimated by taking national accounts totals for each industry and allocating them to regions using the best available local indicators, such as business survey data, employment, earnings and administrative sources; it is therefore partly an apportionment exercise rather than a direct measurement of local output.

Household disposable income is constructed differently: national level household-account totals are broken into components such as wages, self-employment income, benefits, taxes and social contributions, then assigned to where people live using sources such as PAYE, self-assessment, DWP benefits data, housing data and population estimates.

Paul Swinney has found some errors in the Greater Manchester productivity data (also derived from the GVA data) that should give us some pause.

But I found in my research that the wages data (used for the Household disposable income statistics) was not particularly robust. Wages figures come from ASHE, an employer survey sampled from PAYE records, which asks employers about the pay and hours of selected employee jobs and uses this to estimate median or average earnings by place. However, using this to compare cities proved next to useless. If I compared cities from 1998 to 2024 then Greater Manchester was by far the strongest performer, with Edinburgh a distant 2nd. However, if I adjusted the dates slightly to 2002-2022 Manchester fell to second bottom, with Edinburgh 3rd bottom.

I have no doubt that there are errors in both sets of data which is what happens when an organisation that accepts it has let standards slip dramatically in recent years tries to put the whole economy into a spreadsheet.

| A guest post by

|

Good well researched and well written piece.

It was the IRA bomb in 1996 that kick-started the city centre's regeneration out of necessity. Unfortunately, the planners ruined Piccadilly Gardens, which was a lovely, large, oasis when I was child in the 60s/70s. It has been halved in size and is now ugly (I've never got over this). Then the Commonwealth Games of 2002 saw massive regeneration, which was always the plan. Some Greater Manchester residents, however, describe Manchester City centre, as an island in a sea of poverty.

This is a very well evidenced and written article that should be a main source for any informed discussion on 'Manchesterism'.

Having said that, I thought that the final concluding comments were a bit unbalanced.

Sure, Manchester needed to embrace the 'intangible economy' and its city centre skyscrapers, build-to-rent boom and associated night time economy fillip, seems to have been reasonably successful to that end - at least on its terms.

The additional gdp and wealth does not seem to have cascaded down to the wider city and sub regional population. however -other than on a limited 'crumbs falling from the table' basis.

The tram connectivity improvenents predated or were concurrent with the boom. Other than bus service reform, mechanisms supporting inclusive growth seems to have been under-developed or ineffective.

It would be instructive to understand the tenant profile of the build to rents - in London such developments are often targeted towards foreign investors, producing limited domestic filtering or housing chain impacts to the ultimate benefit of local people.

Also not clear whetber sticking and obtaining at least 20 per cent affordable could have been achieved withoot preventing the development - perhaps Leese and Bernstein voulf and should have negotiated harder for Manchester.