Is there a case for a Windfall Tax on North Sea Oil and Gas?

The case for permanently higher taxes on the North Sea

Rishi Sunak has been having a tough time of late. His reputation as the ‘whatever it takes’ chancellor took a beating at the Spring Statement when his response to surging energy and fuel costs fell short of expectations. At the time, Keir Starmer’s Labour had an attractive attack line: Oil and gas producers are receiving an unexpected windfall due to Russia’s invasion of Ukraine, so tax their profits more to fund broad-based tax cuts for consumers and targeted support for people on Universal Credit.

Sunak initially rejected Labour’s argument on the grounds that it would discourage investment in North Sea oil and gas extraction, which in turn would keep prices higher for longer and strengthen Putin’s hand.

More recently, Sunak’s changed his tune somewhat and is now threatening to hike taxes on North Sea profits unless oil and gas producers commit to boosting investment. This view puts him at odds with Business Secretary Kwasi Kwarteng who recently told Sky News: “I’ve never been a supporter of windfall taxes. I think it discourages investment and the reason why we want to have investment is because it creates jobs, it creates wealth and it also gives us energy security.”

Kwarteng’s argument is echoed by trade bodies such as Offshore Energies UK who have warned a windfall tax would deter investment. But they would say that, wouldn’t they? So, who should you believe and what does economics tell us about windfall taxes?

Sunak’s empty threat

First things first, whatever the merits of a windfall tax may be, it is not possible for the Chancellor to threaten businesses into investing more. It is a classic case of the free-rider problem. It might be rational for the North Sea oil and gas sector as a whole to agree to invest more if it discourages the Chancellor from imposing a supertax; but sectors do not make investment decisions. Individual businesses do. You can thank anti-cartel legislation for that. BP will simply not invest to cut Shell’s tax burden.

Windfall taxes are efficient, in theory

Arguments around windfall taxes typically focus on fairness. In other words, are profits due to Putin’s warmongering deserved? But, theories of just desert make for bad tax policy. I’m sympathetic to the idea that high earners owe much of their success to factors entirely out of their control, such as upbringing, genetics, and the fact they are alive in a time of historically unprecedented wealth and stability. But, if we were to effectively impose a maximum income by taxing all earnings above say £80,000 a year we would quite swiftly encounter major problems.

Instead, we should focus on how tax policy affects the behaviour of businesses and individuals. Economists typically describe a tax as more or less efficient based on how much individuals change their behaviour in response. The exception to the rule being when a tax discourages harmful behaviour such as pollution or congestion.

Efficiency isn’t the only consideration for policymakers – the Community Charge (Thatcher’s Poll Tax) was efficient in this sense, but highly regressive – but it is an important one.

A one-off unexpected windfall tax does well on this criteria. As it is one-off, it doesn’t affect future behaviour. And because it’s unexpected, businesses won’t have changed behaviour in anticipation.

There’s one hitch. The tax has to be credibly one-off. If firms expect future windfall taxes then it will inevitably factor into their investment decisions. There’s also a risk that windfall taxes in one sector will have knock-on effects in others. If I make PPE, I might reasonably expect to be hit the next time a pandemic comes around. This is a problem if it discourages stockpiling and building in excess production capacity in preparation. This can be such a problem that it justifies blatantly protectionist and anti-competitive legislation.

However, this doesn’t seem to have been a problem with the UK’s recent windfall taxes. But as oil drillers know better than most, there are only so many times you can go to the same well.

Natural resources are different.

But whether or not the tax is one-off or permanent might not actually matter in the case of North Sea oil and gas.

Profits from North Sea oil and gas production are ring-fenced from other activities and taxed under a separate system. Why? Because natural resources are different. When Tesla is choosing where to locate its next gigafactory, Elon Musk must consider a range of factors. Corporation Tax will be one of them. All things being equal, he will locate in the jurisdiction with lowest corporate taxes (or in practice, the most generous tax credits).

When it comes to North Sea drilling operations, Shell doesn’t have the luxury of shopping around for tax incentives. As long as it is profitable to drill, they will go wherever the oil is.

What matters to Shell (or BP) is not the headline rate, but rather, what exactly is taxed. Specifically, they care about the generosity of allowances for exploration, investment, and decommissioning. If Shell can deduct the full value of the costs of those activities from their taxable income and they can write-off any losses they incur against past taxes, then all profitable North Sea investments will be made. The headline rate is irrelevant.

In other words, if you want to maximise tax receipts from North Sea drilling operations then you should marry a generous investment regime with a high headline tax rate.

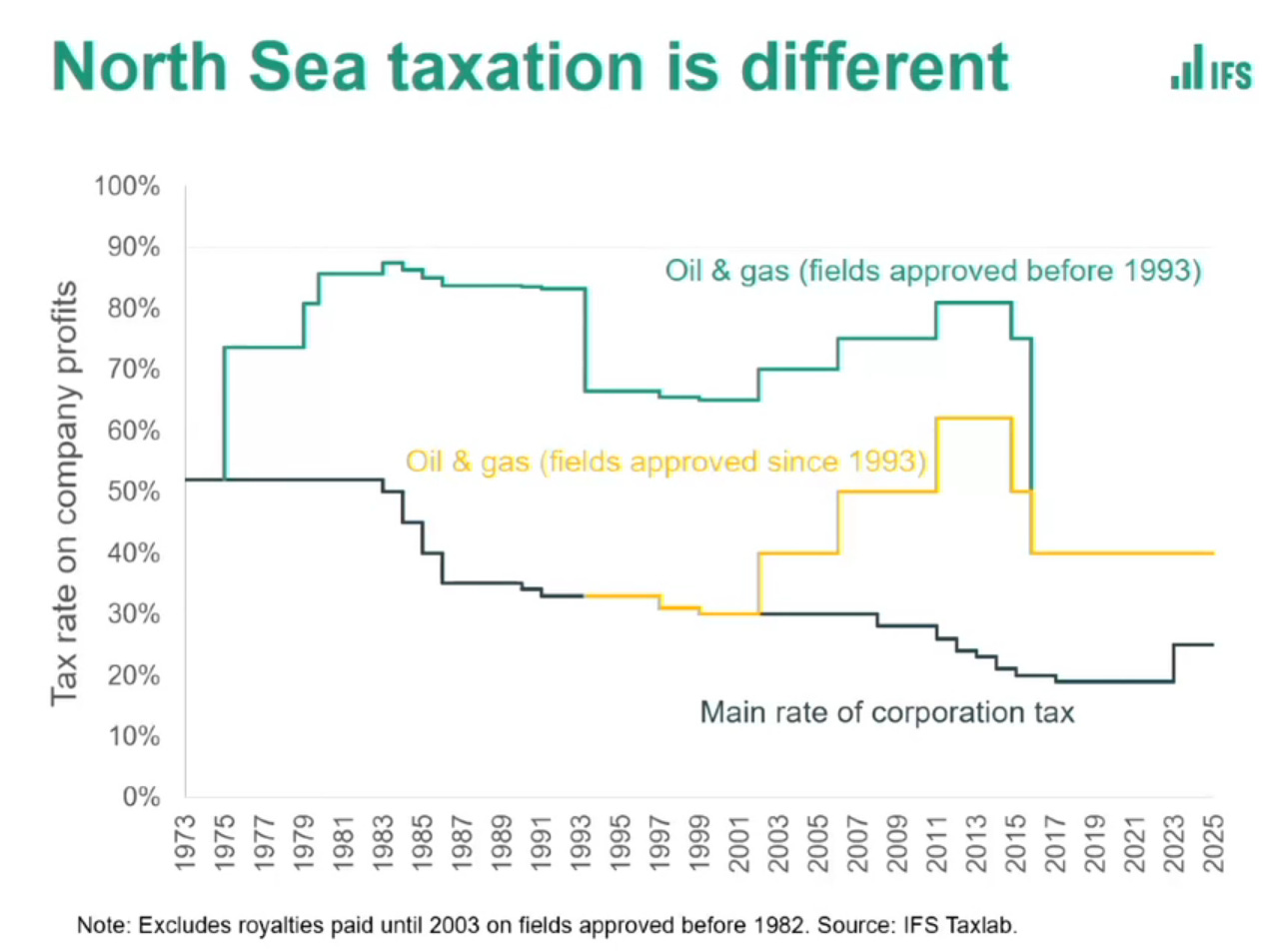

Funnily enough, that’s basically what we already do. North Sea Oil and Gas operations are ring-fenced, granted generous investment allowances (slightly too generous according to Stuart Adam at the IFS) and taxed at a higher rate (30% plus a 10% surcharge). Plus, to account for the inherent risk in oil and gas exploration, producers can carry back any losses they incur against taxes paid since 2002. Recently, this has meant that tax receipts from the North Sea have been low and were briefly negative.

By the way, this is also a reason to be sceptical of climate campaigners who describe tax relief for decommissioning costs as a subsidy.

The case for permanently higher taxes on the North Sea

All of this makes the oil and gas industry’s concerns around a windfall tax deterring investment seem rather unpersuasive.

Regulation is likely to be a bigger driver of differences in investment in the North Sea between Norway and Britain. Norway appears to be more than happy to grant licences for oil and gas exploration, while the UK is more reluctant because further exploration is seen as inconsistent with the move to Net Zero. However, the recently published British Energy Security Strategy includes a commitment for a new licensing round in the Autumn.

It is worth noting that Norway, which has seen substantially more investment in the North Sea over the past decade, also levies a substantially higher tax on profits (78%) from North Sea oil. And as Stuart Adam from the IFS pointed out in a recent lecture, taxes on North Sea profits are relatively low by historical standards – the rate never dropped below 80% under Thatcher.

The strongest case against a one-off windfall tax on North Sea profits is not that it will deter investment, but rather that there is no need for it to be one-off.

P.S.

There is an implicit assumption in this post that increased production in the North Sea is desirable. It is fair to object on the grounds that further production will make it harder to get to Net Zero by 2050.

My response is threefold:

In the short-to-medium term, more North Sea oil and gas production means less money to fund Russian warmongering.

If we want to reduce emissions, carbon pricing is the most cost-effective way to achieve our goals.

Any tax receipts from North Sea oil and gas can be used to fund the transition to a fossil fuel-free economy. More funding for R&D to make cleaner sources of energy cost-effective is a particularly attractive option as it allows countries to sidestep the trade-off between economic growth and decarbonisation.