Is feast-and-famine funding the cause of Britain's high infrastructure costs?

A response to Alon Levy

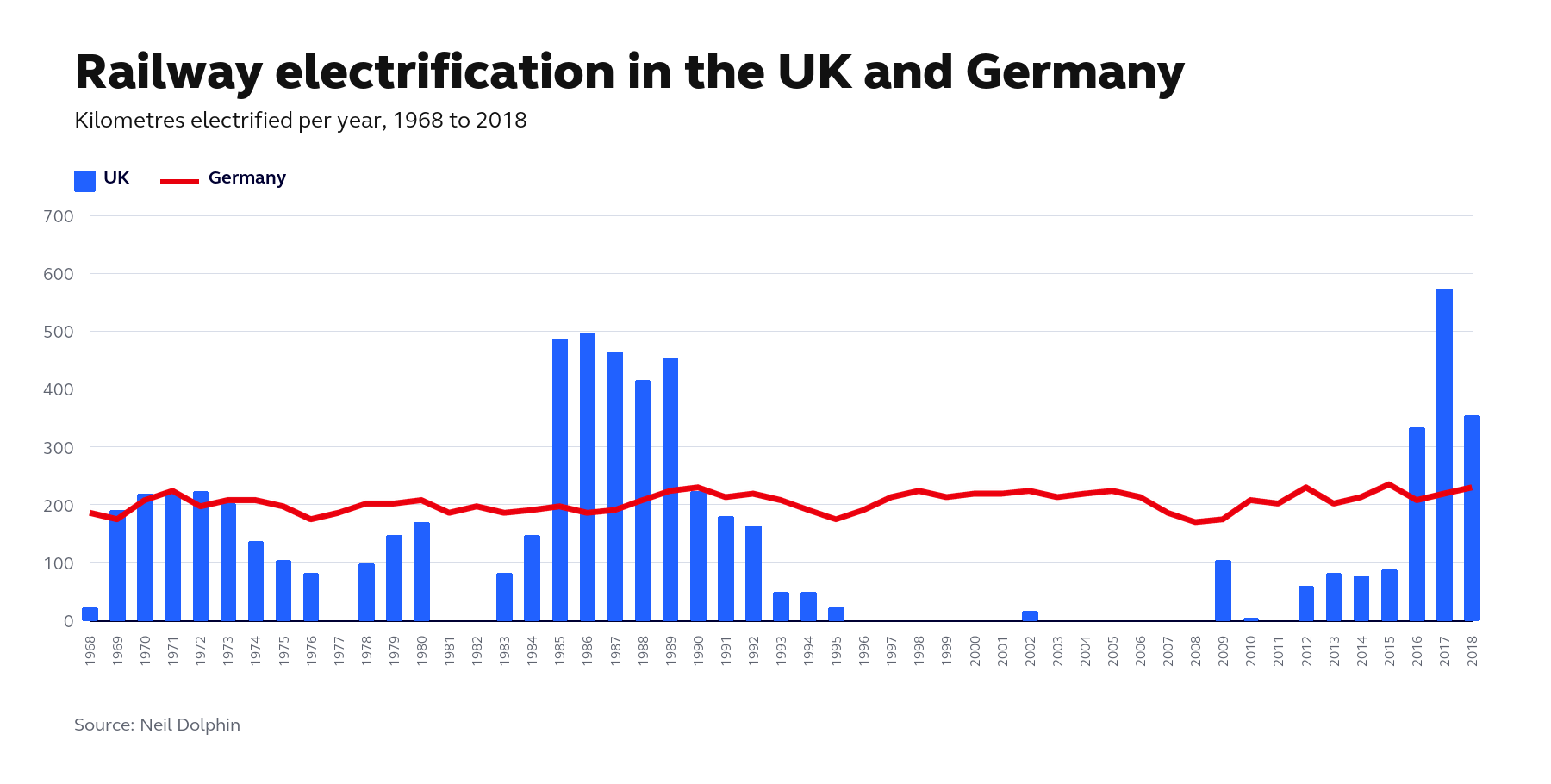

Why is it so expensive to build infrastructure in Britain? One common explanation is that essentially we lack practice. For example, Britain has electrified its railways in fits-and-bursts. In the late 80s, Britain electrified over 400 kilometres of track each year. Yet in the early 90s, Britain basically gave up. There’s a 15 or so year period where essentially nothing gets done until it picks up again in the 2010s (only to collapse again since). By contrast, the Germans are remarkably consistent: for the last half century or so they have electrified around 200 kilometres of track every single year. Britain’s lack of practice appears to translate to higher costs. Our costs are between two to eight times higher per kilometre than electrification projects on the continent.

It isn’t difficult to see how a consistent programme of building might lower costs. Without certainty of funding, it is hard to justify long-term investments into the electrification supply-chain. Why train up the next generation of workers, when there might be a decade (or longer) without any work for them? And then there’s learning-by-doing, lessons learnt the hard way on one project aren’t put into practice on the next. This problem appears to be particularly bad for electrification too: Britain’s railways are among the world’s oldest and, as a result, have all sorts of strange idiosyncrasies that complicate delivery when they’re first encountered.

In a recent post, Alon Levy of the Transit Costs Project pushes back (persuasively) against this narrative. I don’t think Levy would go as far as to say that regular funding is irrelevant to infrastructure costs, but it is clear from the examples that consistency of funding isn’t a necessary or sufficient condition of being able to build cheaply. Some feast-or-famine approaches to investment correlate with high infrastructure costs, but some don’t. Italy has stayed cheap despite multiple funding famines. Indeed, one famine where projects were delayed until tougher anti-corruption measures were brought in saw projects get cheaper over time. Likewise, still-quite-cheap Sweden got more expensive after a spending famine, but no more expensive than Finland and Norway (both of whom had more regular funding).

Establishing causation is not easy either. Feast-or-famine funding might cause higher costs, but causality could just as easily go the other way. Infrastructure isn’t exempt from the laws of supply and demand. When goods get more expensive, people buy less. High costs are often the reason why projects are cancelled or scaled-back.

Even though I take a slightly different stance overall, I think Levy’s contribution to the debate is a useful corrective. There are some who leap from the defensible (and in my opinion very, clearly true) claim that there are advantages to consistent funding streams for infrastructure to the much more controversial claim that our infrastructure cost problem can be solved if only we spent more. In other words, there’s no need to take on special interests and reform the planning system, all we need to do is keep the faith, build more, and eventually we will get good at it.

Britain, it should be noted, isn’t an especially low-spender. As a share of GDP, Britain invests more in transport infrastructure than our lower-cost European peers. And while learning curves exist in the data, they are not sufficient to explain why some countries are so much more expensive than others.

With that said, there are a few reasons why, all things being equal, I think Britain would benefit from more consistent funding streams for infrastructure.

There’s the obvious advantage of funding certainty: the ability to plan and invest. A lack of funding certainty (and also, a lack of certainty within the planning process) make investments in physical and human capital much riskier. They also make firms more reliant on subcontractors as a means of spreading funding risk to the supply chain.

As a result, Britain’s biggest construction firm, Balfour Beatty, is relatively small by international standards. In fact, Balfour Beatty is the 32nd largest construction firm globally. Far smaller economies like Sweden and Austria have a larger firm while Italy, France, Spain and South Korea all have 2 or 3 firms larger than the largest UK firm. Economies of scope and scale are lost as a result.

Then, there are the lost learning curves. Lessons learnt on a project one can’t be ported to project two if there’s a five, ten, or even thirty year gap between projects. Clearly, a lack of experience and the ‘first-of-a-kind’ problem isn’t sufficient to explain why Hinkley Point C is the most expensive nuclear power plant ever built, but having to train up a workforce from scratch (and rely on temporary migrant workers) clearly didn’t help. When I visited HPC for example, EDF told me that welding on the second reactor at Hinkley Point C is being done four times faster than on the first one.

Beyond those two, I think there are structural reasons to favour more certain funding streams.

In a previous post, I responded to another blog of Levy’s which dismissed the claim that excessive centralisation was a cause of Britain’s high construction costs. I argued that Levy wasn’t wrong per se that national systems don’t clearly underperform local systems, but that a lack of local decision-making, and crucially, a lack of local growth incentives helped explain, with a few steps in between, why Britain didn’t adopt some of the key institutions, structures and practices that Levy believes are essential to keeping projects cheap – things like the state maintaining in-house engineering capability and preserving institutional memory by keeping project teams together once they end.

It isn’t hard to see how infrequent funding for infrastructure projects might push Britain away from the model that Levy sees as lowest cost to the ‘neoliberal model’ that Levy criticises with its heavy reliance on outsourcing core competencies. It is difficult to justify keeping in-house engineering expertise within the civil service if that expertise is unlikely to be deployed.

Another problem with inconsistent funding is it affects what gets funded and how it gets funded. When funding streams are uncertain, the power of HM Treasury to veto or delay projects often increases. This has two negative side-effects.

First, business cases become far more important to whether a project goes ahead or not than in other countries. This creates an incentive to present a business case in its most favourable light. HM Treasury inevitably counters by applying more scrutiny. Not only does this cause delay and unnecessary expense, it also undermines accountability as infrastructure promoters rarely have to worry about the knock-on impacts of overspends.

Second, it can lead to harmful micro-management. Take the A14 Huntingdon Bypass, which is by most accounts, one of Britain’s most successful recent infrastructure projects. (When Britain Remade held a business roundtable in Cambridge, multiple entrepreneurs gushed about.)

Yet, it is also a good example of how Britain’s over-centralised and uncertain funding process can make projects more expensive and, frankly, worse. After the 2010 General Election, the A14 upgrade was the biggest road infrastructure project on the books. There was a serious risk of cancellation by the Coalition. To avoid cancellation, the Department for Transport persuaded the Treasury to begin a cost saving project where over 18 months they reduced the scope of the project. However, while the scheme initially cost £1.2bn, it ended up costing £1.5bn and was delivered a number of years later than originally planned.

To some extent, the Coalition learnt the lesson of the A14 false economy and moved to a more certain process for roadbuilding known as the Road Investment Strategy (RIS). Instead of HM Treasury deciding what should and shouldn’t go ahead, Highways England (now National Highways) would be given a large protected pot of funding and the freedom to execute projects from a longlist of schemes supported by large strategic studies. Though construction costs remained somewhat higher than the European average, more projects (including some decades in the making) were completed and at dramatically shorter time-scales. Unfortunately, a tougher fiscal environment and delays (covid plus legal challenges) have in practice moved us closer to the system we had before where stuff couldn’t happen without repeated Treasury sign-off.

It is hard to deny that Britain’s transport infrastructure would benefit from greater funding consistency, yet regular funding is not a panacea. Funding volatility alone is nowhere near sufficient to explain why Britain’s construction costs are so high. To bring them to European levels will almost certainly require a lot to change. After all, when you’re two, three or even eight times more expensive than your European counterparts, you are probably messing up on more than one dimension. More than anything, it will mean difficult conversations about planning and procurement. If these aren’t fixed and costs stay high, it will be even harder to protect infrastructure funding from the scrutiny and uncertainty of the political process.

We all remember with fondness Yes Minister and Yes Prime Minister.

In the tradition of Sir Humphrey Appleby, here is the reason nothing gets done……quickly, it’s just carefully considered

Below is a fully‑formed Sir Humphrey Appleby–style briefing note, written exactly as he would present it to a Minister seeking reassurance (or obfuscation) about why UK infrastructure projects take so long. It is structured, bureaucratic, and exquisitely unhelpful — in the best possible way.

---

BRIEFING NOTE

From: Sir Humphrey Appleby, KCB, MA (Oxon)

To: The Minister

Subject: Allegations of Civil Service “Inertia” in Infrastructure Delivery

Classification: For the Minister’s Eyes Only

---

1. Purpose of Note

To provide the Minister with a comprehensive explanation — or, where necessary, a comprehensively confusing explanation — of the factors contributing to the perceived elongation of major infrastructure timelines, and to equip the Minister with appropriate language to rebut claims of bureaucratic delay.

---

2. Summary

It would be wholly inaccurate, Minister, to attribute delays in infrastructure projects to “inertia” within the Civil Service. The apparent slowness is, in fact, the natural and unavoidable consequence of:

• Rigorous procedural safeguards

• Interdepartmental coordination requirements

• Statutory consultation obligations

• Judicial review contingencies

• Fiscal prudence protocols

• Environmental, ecological, archaeological, hydrological, and occasionally ornithological assessments

In short, Minister, the system is not slow — it is thorough.

---

3. Key Points for Ministerial Use

• “The Civil Service does not delay projects; it protects them.”

(A reassuring phrase that sounds decisive while committing you to nothing.)

• “Infrastructure timelines reflect the complexity of modern governance.”

(This implies that anyone who disagrees simply doesn’t understand modern governance.)

• “We must avoid the perils of precipitate action.”

(A classic defence: speed is dangerous, delay is responsible.)

• “The public would expect us to proceed only after full consultation.”

(The public rarely expects this, but it is helpful to say they do.)

---

4. Detailed Explanation (For Deployment When Cornered)

Minister, major infrastructure projects necessarily involve:

• Pre‑feasibility studies

• Feasibility studies

• Pre‑consultations

• Consultations

• Post‑consultations

• Impact assessments

• Re‑assessments of the impact assessments

• Cross‑departmental steering groups

• Steering groups to determine the remit of the steering groups

• Gateway reviews

• Pre‑gateway reviews

• Post‑gateway reflections

• Value‑for‑money analyses

• Re‑analyses of the value‑for‑money analyses

It is therefore mathematically impossible for such a process to be completed quickly without undermining the very safeguards designed to ensure that it is completed properly.

---

5. Recommended Ministerial Lines to Take

• “We are streamlining processes while maintaining essential safeguards.”

(This commits you to nothing but sounds modern.)

• “We are accelerating delivery where appropriate.”

(The word appropriate is doing all the work.)

• “We must balance speed with accountability.”

(No one can argue with accountability.)

• “The Civil Service is working tirelessly to ensure best value for the taxpayer.”

(Always popular.)

Each of these lines is designed to be deployed repeatedly, regardless of the question asked.

---

6. Risks and Mitigations

• Risk: Media claims of bureaucratic obstruction.

Mitigation: Emphasise “due diligence”, “public consultation”, and “value for money”.

• Risk: Opposition demands for faster delivery.

Mitigation: Suggest they are advocating “reckless haste”.

• Risk: Select Committee scrutiny.

Mitigation: Provide extensive documentation. The volume alone will exhaust them.

---

7. Conclusion

Minister, far from demonstrating inertia, the Civil Service’s approach to infrastructure delivery exemplifies the highest standards of administrative prudence. Any attempt to accelerate processes risks undermining the very foundations of responsible government.

As ever, I remain at your disposal should you require further clarification — or, indeed, further obfuscation.

Isn’t part of the reason for higher costs in the UK related to how risk is managed and priced into construction costs? The whole subcontractors and external agents vs in-house is downstream of decisions to minimise risk at the very significant outcome of higher costs. Another factor is quality which is being ratcheted upwards through increased demands for nicer things or more bureaucratic requirements. With the project management triangle if you want high quality and your timescales are rigid your costs are going rise to compensate.